Netherlands Budget Proposals

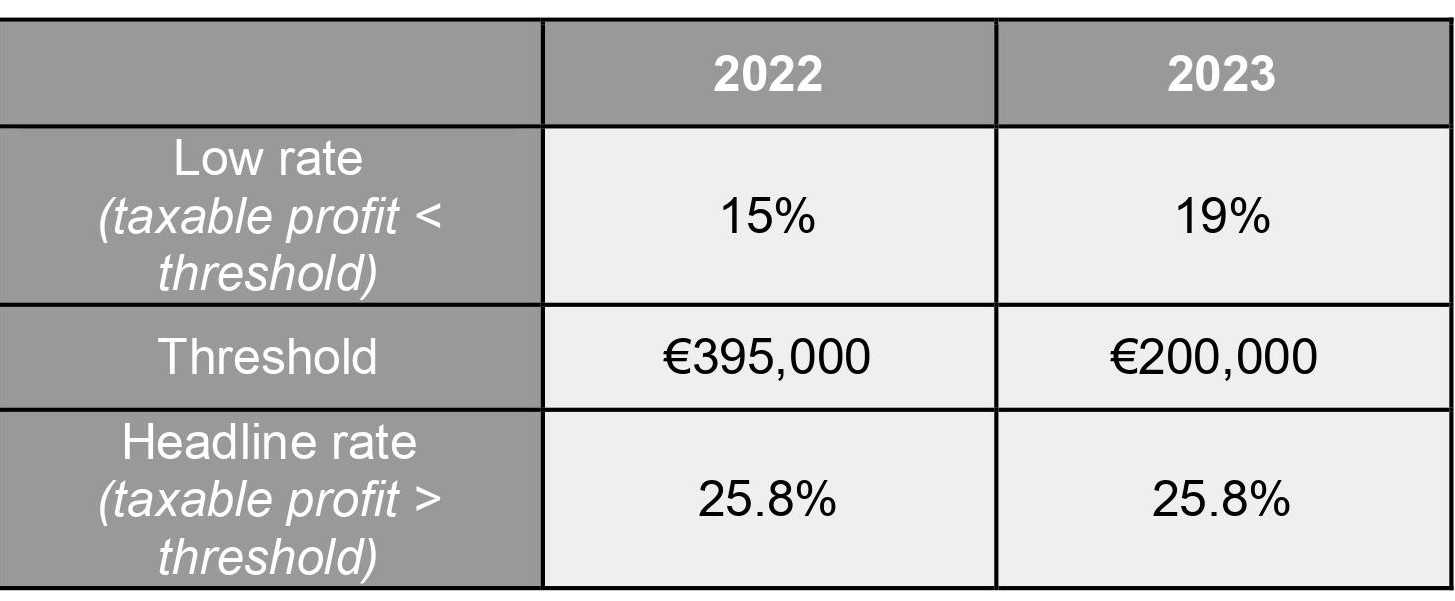

Corporate Income Tax (CIT) rate – [Budget Day Proposal]

Effective date: 1 January 2023

Among others to finance government spending, the step-up CIT rate will be increased from 15% to 19% and the 25.8% headline CIT rate will start applying to taxable profits above €200,000.

Cap on 30%-facility for expatriates – [Budget Day Proposal]

Effective date: 1 January 2024

Special tax benefits exist whereby qualifying expatriates can receive a reimbursement of costs of 30% of their salary (irrespective of actual costs incurred). It is proposed to cap the salary basis to which the 30% is applied to the so-called “WNT-norm” (€216,000 in 2022, adjusted annually).

It is furthermore proposed to explicitly include in legislation that employers/employees can opt for either reimbursement of actual costs or the 30%-facility on a year-by-year basis. Certain transition rules can apply for a period of two years.

Fiscal investment funds holding real estate – [Budget Day Proposal]

Effective date: 1 January 2024

Key takeaway: taxpayers should monitor details of upcoming legislative proposal.

A special regime exists for qualifying fiscal investment funds (FIF) that are – as a result of such regime – taxed against a 0% CIT rate. In instances where such a FIF (predominantly) invests in real estate, the Government found that foreign investors holding an interest in the FIF are oftentimes effectively not taxed on income or proceeds earned from that real estate through the FIF (no CIT nor WHT).

A key element of the proposed changes is that a FIF would no longer be allowed to directly invest in Dutch or foreign real estate in order to keep its FIF status (and hence benefit from the 0% CIT rate). Further details will be published as part of the 2024 budget proposals.

Other key legislation/expected legislative proposals

Dividend Withholding Tax (WHT) changes – [Earlier Proposal from May 2022]

Effective date: 1 January 2023

Three changes are proposed to the dividend WHT legislation as follows:

1) Currently a Dutch NV or BV can request the tax inspector to confirm the amount of paid-up share capital for dividend WHT purposes through a decision eligible for appeal. It is proposed to also extend this possibility to other types of entities that are withholding agents (e.g., Dutch Cooperatives).

2) Reimbursements for capital contributions by shareholders, members, participants or other beneficiaries and reimbursements on profit-participation-loans (qualifying as equity) are currently not explicitly mentioned as taxable events for dividend WHT. The proposal ensures that such reimbursements are in fact taxable events for dividend WHT.

3) In the anti-dividend stripping provisions the term “legal entity” is currently used, suggesting that entities without legal personality (such as partnerships) that qualify as non-transparent for Dutch tax purposes are not in scope of the anti-dividend stripping provisions. The term “legal entity” is therefore proposed to be amended to “entity” in order to also bring these particular entities explicitly in scope (provided other conditions are met).

Alignment of legal entity and partnership classification rules with international tax standards – [Announced Proposal]

Effective date: expected as of 1 January 2024, updated legislative proposal expected in Spring 2023.

Key takeaway: taxpayers should initiate conversation on the potential implications for the Dutch qualification of (foreign) entities/partnerships in their legal structure (while also monitoring legislative progress).

On 29 March 2021, the Dutch Government released a draft proposal for public consultation to revise the Dutch classification rules for entities incorporated under foreign law and partnerships/funds formed under Dutch as well as foreign law. The proposed new entity classification rules are intended to be better aligned with international tax standards. It is expected that this will result in a reduction of potential hybrid outcomes due to mismatches in entity classifications between the Netherlands and foreign jurisdictions.

WHT on dividend payments to low-taxed jurisdictions, hybrid entities and in abusive structures – [Already enacted]

Effective date: 1 January 2024

Key takeaway: taxpayers should assess the impact on dividend payments by Dutch withholding agents in their organizational structure.

On 11 November 2021, the Bill to introduce the WHT on dividend payments to low-taxed jurisdictions, hybrid entities and in abusive structures was enacted. This is an extension to the WHT on interest and royalty payments to low-taxed jurisdictions, hybrid entities and in abusive structures, that applies as from 1 January 2021. The WHT rate is equal to the headline CIT rate (currently 25.8%).

This WHT will exist next to the “normal” dividend WHT of 15%. However, an anti-cumulation rule will apply, limiting the total dividend WHT on relevant payments to low-taxed jurisdictions, hybrid entities or in abuse structures to 25.8% (with the expectation that less hybrid entities will exist under the new classification rules – see previous paragraph). The implications of this legislation must be carefully assessed on a case-by-case basis and could impact certain taxpayers that today are not subject to (the withholding of) dividend WHT.

Key EU initiatives – what to consider right now?

Key takeaway: taxpayers should initiate conversation on the potential implications and take EU initiatives into consideration for upcoming transactions/restructurings (while also monitoring legislative progress).

UNSHELL / 3rd EU Anti-Tax Avoidance Directive (ATAD3) – [Proposal]

Introduction of an EU-wide “substance test” to prevent misuse of EU undertakings for obtaining tax advantages. The originally proposed effective date is 1 January 2024, although the EU is discussing postponement to 1 January 2025.

EU Pillar Two Directive – [Proposal]

Implementation of the Organisation for Economic Co-operation and Development’s Pillar Two initiative to ensure a global minimum tax of 15% for multinational enterprises (MNEs). The proposed effective date is accounting periods starting on/after 31 December 2023 for the Income Inclusion Rule (IIR) and 31 December 2024 for the Undertaxed Payments Rule (UTPR). Certain transition rules can already impact intercompany asset transfers after 30 November 2021. Pending unanimous consent among all EU Member States, a joint statement by France, Germany, Italy, Spain and the Netherlands was released on 9 September 2022 to underscore their commitment to the proposal and timeline (even if unanimous consent would not be reached).

Debt-Equity Bias Reduction Allowance (DEBRA) – [Proposal]

Aimed at encouraging equity funding through a notional deduction on equity and a (further) restriction of deductible interest expenses. Proposed effective date is 1 January 2024.

EU Public Country-by-Country Reporting (CbCR) – [Adopted]

Public disclosure of income taxes paid and other tax-related information such as a breakdown of profits, revenues and employees per country for MNEs with a consolidated revenue exceeding €750M in the last consecutive two years. Effective date is financial years starting on/after 22 June 2024.

EU temporary solidarity contribution – [Proposal]

An EU-wide temporary “solidarity contribution” or “windfall tax” levied at a rate of at least 33% on surplus taxable profits of companies active in among others the oil, gas, refineries and coal sectors. It will apply for one year, being the fiscal year starting on or after 1 January 2022.